AI-Initiated Payments and Fintech Readiness: Key Findings

- AI has successfully initiated secure payments, signaling a major shift from advisory to executional roles in fintech systems.

- Traditional fintech architectures are not AI-native, making them ill-equipped to support machine-initiated transactions at scale.

- Custom platforms must embed trust-driven automation, requiring new authorization models and APIs designed for intelligent agents.

Since the inception of digital payments, one thing has always remained - the need for a person to start every transaction. However, that is starting to change.

Late last year, Visa revealed that it had completed hundreds of secure transactions initiated entirely by AI agents.

This milestone signals more than incremental innovation. It marks the early arrival of autonomous commerce, where intelligent systems can act on behalf of users to complete financial actions.

Malay Parekh, CEO of leading global software development firm, Unico Connect, says that as AI agents move from recommending purchases to initiating payments, enterprises involved in building custom fintech platforms are faced with a fundamental question.

“Are their systems designed for a future where software, and not people, trigger transactions?” Parekh asks.

Editor's Note: This is a sponsored article created in partnership with Unico Connect.

The Numbers Behind Autonomous Finance

To understand the payment ecosystem and the influence of AI-initiated payments, it helps to take a look at how global payment systems and technology are evolving.

Insights from McKinsey’s Global Payments Report highlight the scale, innovation, and readiness of today’s payments landscape:

- As of 2025, the global payments industry generated approximately $2.5 trillion in revenue, showing just how large and economically important the sector has become.

- Around 3.6 trillion payment transactions were processed globally last year, highlighting the massive volume of financial activity that modern systems handle every day.

On the AI front, insights from Digital Silk suggest that:

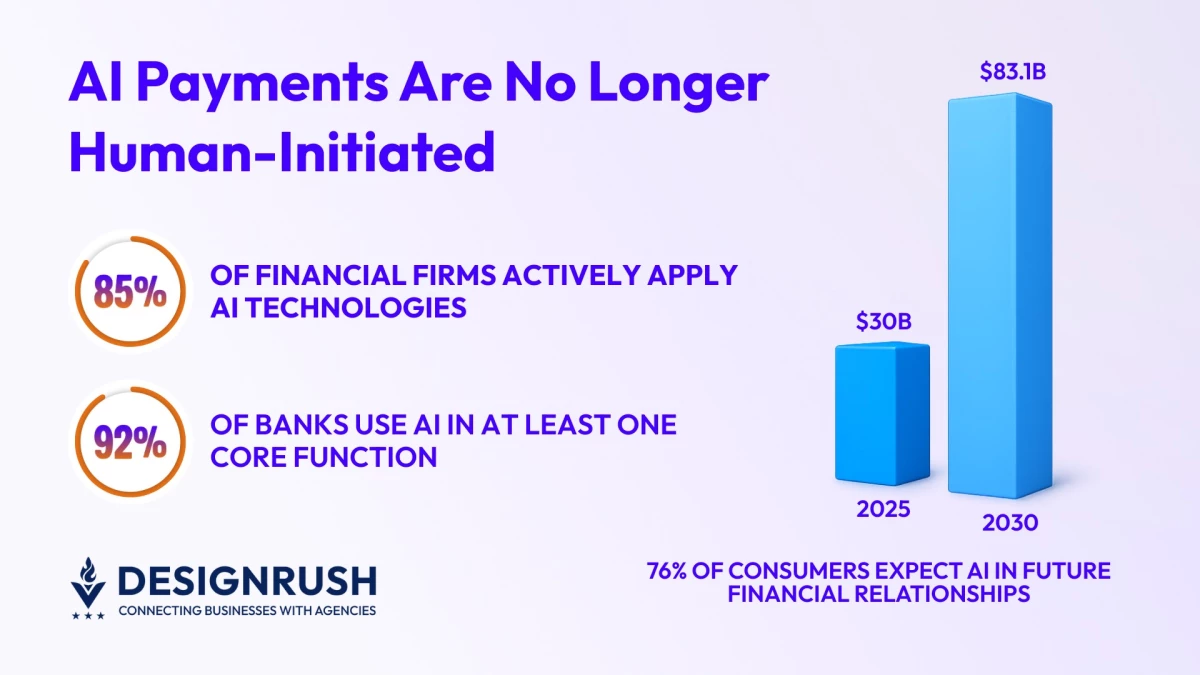

- AI in the fintech market is set to grow from $30B in 2025 to $83.1B by 2030, making AI adoption a key competitive differentiator.

- The use of Gen AI in the banking and finance sectors is projected to grow from $1.29 billion in 2024 to $21.57 billion by 2034, underscoring how generative models are becoming foundational to future financial service design and automation.

Moreover, additional global data points reinforce just how deeply AI is embedding itself across both institutions and consumer expectations:

- Over 85% of financial firms are actively applying AI technologies, primarily across fraud detection, operations, and risk modeling functions.

- 92% of banks worldwide reported active AI deployment in at least one core function, signaling near‑universal adoption across essential financial workflows.

- 76% of consumers believe that AI will be a standard part of their financial services relationships within five years, reflecting growing user expectations and normalization of AI‑driven financial interactions.

“Together, these numbers illustrate a payments ecosystem that is perfectly positioned to support the rise of secure, AI-initiated transactions like those pioneered by Visa,” Parekh says.

From Human Checkout to Agent-Initiated Transactions

Visa’s announcement confirms what many fintech leaders have anticipated.

AI is no longer limited to assisting consumers or flagging risks behind the scenes. It is beginning to act.

In Visa’s pilot environments, AI agents interpreted user-defined rules, authenticated authorization, and initiated payments securely. This represents a shift from AI as an advisory layer to AI as an execution layer. And the difference is profound.

“Execution requires trust,” Parekh says. “It requires systems that can validate intent, enforce limits, and ensure accountability without a human approving each step.”

This is where payment infrastructure, AI governance, and fintech architecture converge.

What This Means for Custom Fintech Development

For fintech builders, the implications are immediate. Platforms designed exclusively around human-initiated flows will struggle as autonomous transactions scale.

To remain relevant, Unico Connect advises that custom fintech systems must evolve in three critical ways:

1. Designing for AI-Native Transaction Logic

Payment engines must assume that an intelligent agent may initiate a transaction. This means embedding rules, context awareness, and delegated authority directly into transaction logic.

2. Rethinking Authorization Models

Traditional authentication assumes a person is present at checkout. Agent-initiated payments require new authorization frameworks that define what an AI is allowed to do, under which conditions, and with what constraints.

3. Building Automation-Ready APIs

APIs must support continuous, machine-driven interaction with pricing, settlement, compliance, and reconciliation layers. Manual checkpoints become friction points in an autonomous world.

“Fintech platforms that treat AI as an add-on will fall behind. Those that embed it at the architectural level will define the next generation of digital finance,” Parekh says.

Preparing for the Future of Autonomous Finance

The question is no longer whether AI will initiate payments. It already has. The real challenge is which fintech platforms will be ready when autonomous finance becomes the norm.

“This future will not eliminate people from the equation, but will redefine how their intent flows through the system. Trust and oversight will not be optional, and they must be architected into every autonomous interaction.

“Because autonomy without control fails. But control without autonomy will limit progress," Parekh says.

Ready to build for the AI payments era?

Take a look at our list of the Top AI Companies of 2026.