X Money's Platform Launch: Key Findings

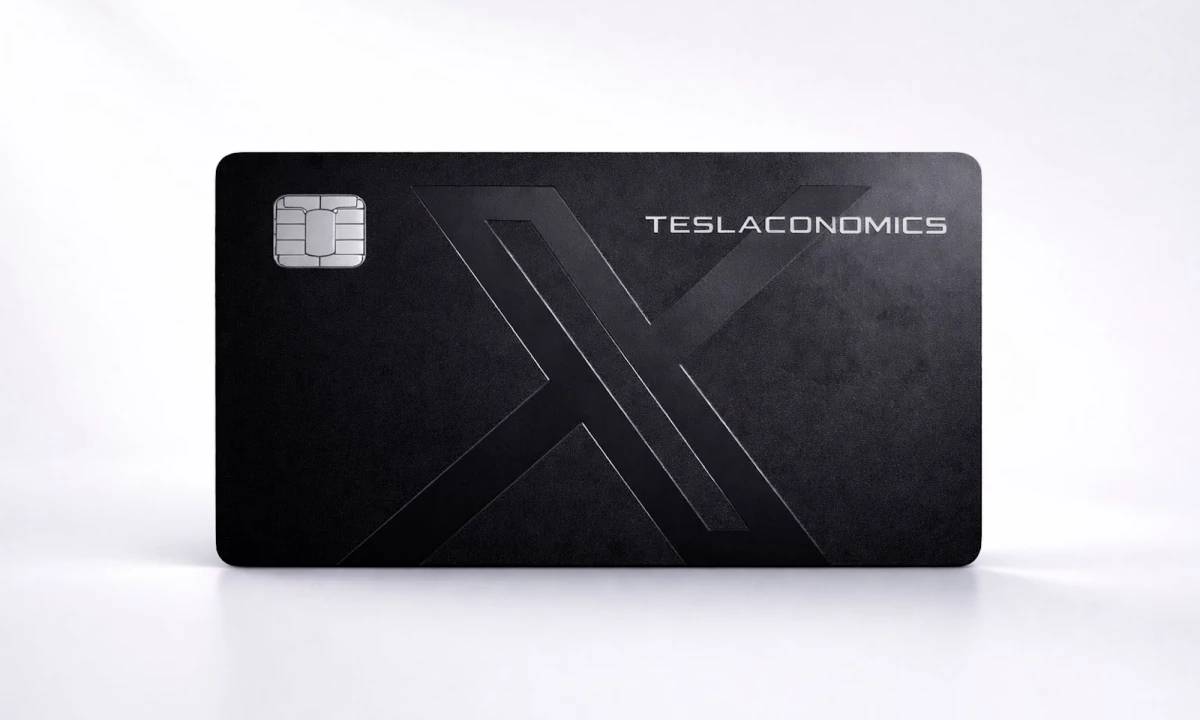

- It has entered a limited beta release with peer-to-peer payments, a 6% APY on deposits, and a personalized metal Visa debit card.

- X holds money transmitter licenses in more than 40 states and has partnered with Visa to support its approximately 600 million monthly active users.

- William Shatner previewed the beta publicly by auctioning 42 invites at $1,000 each for charity, generating organic conversation without a formal campaign.

X is moving closer to becoming a payments platform, and Elon Musk claims it will be "big."

The social media company, owned by Musk, has begun a limited beta rollout of X Money.

𝕏 Money early public access will launch next month

— Elon Musk (@elonmusk) March 10, 2026

It's slated to be a financial feature that lets users send money, earn interest on deposits, and make purchases through a dedicated Visa debit card.

The beta was also promoted publicly by "Star Trek" actor William Shatner, who shared screenshots of the interface.

He also auctioned off 42 beta invites at $1,000 each, with proceeds going to his charity supporting children's and veterans' organizations.

View this post on Instagram

The feature currently advertises a 6% annual percentage yield on deposits, well above most traditional savings accounts.

The launch puts X in direct competition with established payment platforms and raises concrete questions for brands already investing in the company.

X's Payments Expansion

Musk has signaled since his 2022 acquisition of Twitter that he wanted to build an "everything app."

This was inspired by China's WeChat, a platform where users manage social activity, payments, and commerce in one place.

X Money is the first concrete step in Musk's vision.

The beta interface includes tabs for account management, activity tracking, and rewards, along with options for deposits, peer-to-peer transfers, and payment requests.

Metal Visa debit cards personalized with each user's X handle are being offered to early access winners, with zero foreign transaction fees attached.

X Money deposits are held by Cross River Bank and insured up to $250,000 per person through the FDIC.

The social media platform, formerly known as Twitter, has also secured money transmitter licenses in over 40 states and registered with the Financial Crimes Enforcement Network.

Its partnership with Visa means the infrastructure is already in place to reach a significant share of the platform's active user base from day one.

That graphic gets around… you know that your Silicon Valley follower types can get in on a beta invitation to X Money by making a donation to my charity. 👇🏻https://t.co/I3A8BLsZQc

— William Shatner (@WilliamShatner) March 6, 2026

Spread the word! 😉 https://t.co/tWcDnPJIoI

The Shatner promotion, while unconventional, has also put the product in front of an audience that might not have been following X's financial ambitions closely.

In turn, it has generated organic conversation about the feature before a full public launch.

The Numbers Brands Need to Know

X reports approximately 600 million monthly active users.

This is a pool that would give X Money an immediate distribution advantage over most standalone fintech apps at launch.

The 6% APY on deposits also compares favorably against the national average savings rate, which has hovered below 1% at most major retail banks.

In the U.S. alone, credit card companies collected $148.5 billion in merchant fees in 2024, according to data from the Nilson Report.

This figure gives context to why a platform-native payments option with lower friction could appeal to businesses already active on X.

Silicon Valley investor Chamath Palihapitiya has publicly noted that if X Money reaches meaningful scale, a user's social profile could become a financial asset in its own right.

Follower count and content engagement are also factored into how financial products are underwritten on the platform.

The idea remains speculative, but it points to where the longer-term product ambition may be headed.

This will be big https://t.co/Xubex9Mea1

— Elon Musk (@elonmusk) March 4, 2026

X Money introduces a new set of brand considerations for those who already use X as an advertising or community channel:

- Commerce and content may converge sooner than expected: It could give brands a direct payment path without routing through third-party checkout.

- Creator partnerships on X carry new financial weight: If followers factor into financial credibility, how brands evaluate influencer deals will need to adjust.

- Early beta engagement has positioning value: Brands that test X Money in promos now will be ahead of the feature before it reaches general availability.

This may very well be the first ice cream 🍨 bought on @XMoney and it was free 🙌🏻because of the Welcome Gift of $25. 😉👍🏻 @elonmuskhttps://t.co/fYbsWhZA0m

— William Shatner (@WilliamShatner) March 9, 2026

Aleksey Gureiev, technical lead at digital product design and development agency Shakuro, told DesignRush that the real complexity for X Money begins after this initial feature rollout.

"Launching payments is only the first layer. Once people actually start using money inside the platform, the product team has to think about developer infrastructure," he commented.

"APIs for merchants, tools for creators to monetize directly, and systems that manage transactions at scale all become necessary. These pieces determine real utility and growth."

Our Take: Is X Money a Serious Contender?

We think that X Money has real force behind it.

This is a payments product with meaningful backing, and the 6% APY is the kind of number that gets attention from users who are already on the platform daily.

The Shatner promotion was an interesting choice, given his recent social media fame. He even did a Super Bowl commercial for Kellogg's Raisin Bran.

It kept the tone light and avoided the kind of corporate announcement energy that tends to land flat on social platforms.

The more interesting question is what happens when X Money reaches general availability, and brands actually start integrating it into their campaigns.

Brands evaluating new payment channels and platform commerce need agencies that understand how financial features interact with social advertising strategy.

Explore the top digital marketing agencies in our directory.